With sports betting apps everywhere and major wagering events like the Super Bowl and March Madness right around the corner, gambling is no longer a niche activity. What many taxpayers don’t realize is that recent federal tax law changes make gambling income — and especially gambling losses — far more punitive starting in 2026.

The One Big Beautiful Bill Act (OBBBA) permanently rewrote the rules under Internal Revenue Code §165(d). While the headline sounds technical, the real-world impact is simple: even gamblers who break even economically may owe tax on “phantom income.”

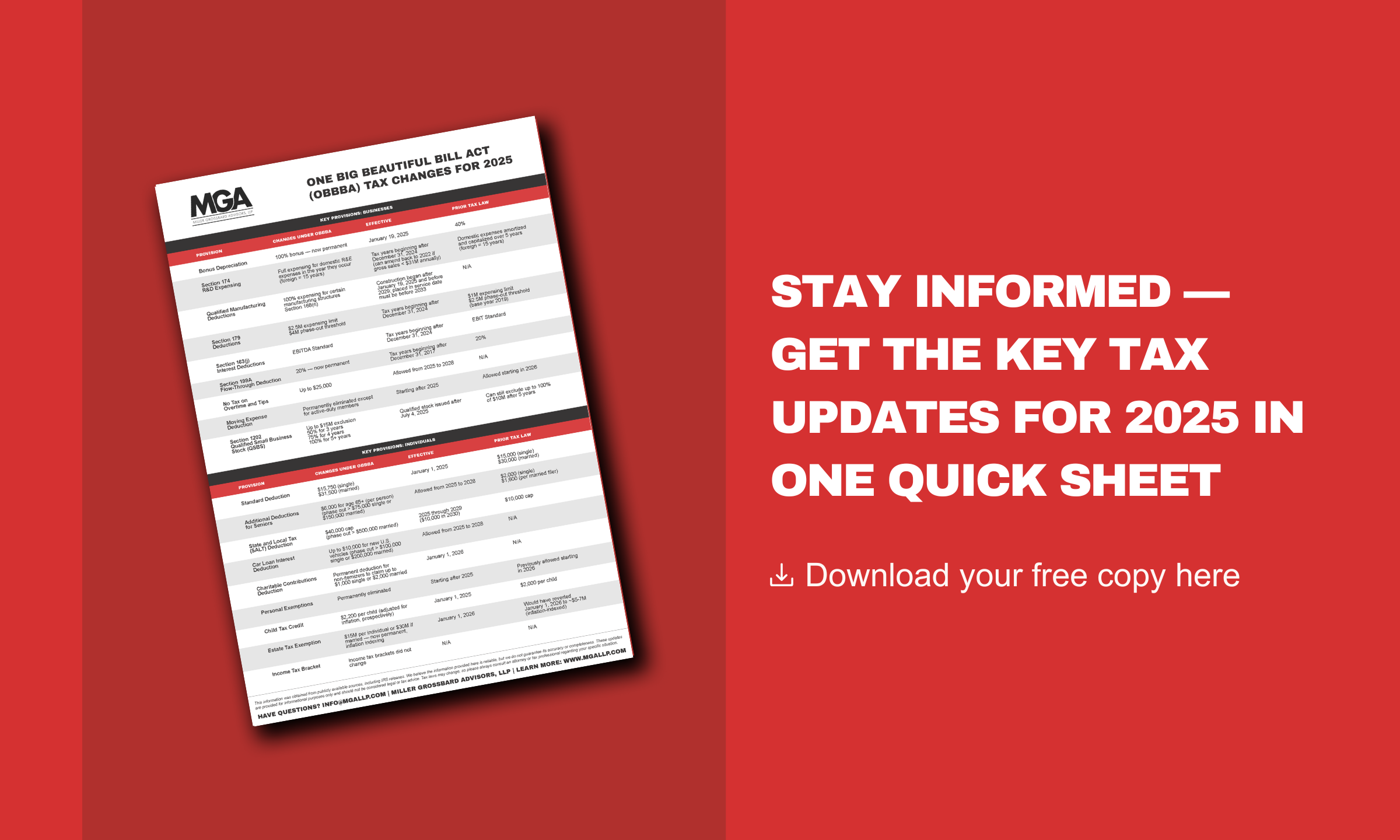

Here’s what changed, why it matters, and what taxpayers should be doing now.

The Old Rule: Losses Could Offset Winnings (But No More)

Under longstanding tax rules, gambling losses were deductible only to the extent of gambling winnings. In practice, that meant:

- If you won $50,000 and lost $50,000, you reported zero net gambling income.

- Casual gamblers deducted losses as an itemized deduction.

- Professional gamblers could deduct related expenses, but after the Tax Cuts and Jobs Act (TCJA) in 2017, those deductions could no longer create a net loss.

Even after the TCJA tightened the rules, a gambler who truly broke even still broke even for tax purposes.

The New Rule: A Permanent 90% Cap on Losses

Starting with tax years beginning after December 31, 2025 (i.e., 2026 and later), OBBBA permanently amended IRC §165(d) to impose two separate limitations:

- Losses are still capped by winnings. This rule didn’t change. Losses can only offset gambling gains.

- Losses are now further limited to 90% of actual losses. This is the big change.

The statute now provides that the deductible amount of wagering losses for a year:

- Equals only 90% of the losses incurred, and

- Is still limited to the amount of gambling gains

In plain English: Even if you lose exactly what you win, you will still be taxed on 10% of your “net” winnings.

Why This Matters: Thin Margins Get Hit the Hardest

This rule is especially punishing for gamblers who operate on small margins, like sports bettors, poker players, and frequent casino patrons.

Example

- Gambling winnings: $100,000

- Gambling losses: $100,000

- Deductible losses (90%): $90,000

Result

- Taxable gambling income: $10,000

- Economic profit: $0

The taxpayer owes tax on income they never actually kept.

How Are Gambling Wins and Losses Measured?

This is where things get murky and risky, because “session” netting still matters.

The Tax Court has long allowed gamblers to net wins and losses within the same gambling session, even if a W-2G reports a single large win. This can produce surprising results:

- A gambler may receive a W-2G

- Yet still have a net loss for that session

Courts have accepted session-based netting, but what counts as a “session” is not clearly defined. Recent cases suggest the IRS and courts may be moving toward:

- A per-establishment approach, or

- A broader annual view for certain activities

This uncertainty matters more than ever because the 90% limitation applies after session netting is determined.

What the IRS Expects From Gamblers

IRS guidance requires gamblers to maintain:

- Date and type of wager

- Gambling establishment and location

- Amounts won and lost

- Supporting records such as: W-2Gs, casino statements, betting tickets, and bank and credit card records

Yes, the guidance even references “names of persons present,” but in practice, contemporaneous, verifiable financial records matter most.

Planning Takeaways Before the Big Game(s)

As major wagering events approach, like the Super Bowl and March Madness, taxpayers should keep a few key points in mind:

- Breaking even is no longer tax-neutral

- High-volume gamblers face higher effective tax rates

- Documentation failures can turn losses into taxable income

- W-2Gs do not tell the full story, but they do alert the IRS

For frequent gamblers, professionals, and anyone wagering significant dollars, this is no longer a DIY tax area.

The Bottom Line for Gamblers in 2026

The OBBBA quietly transformed gambling into one of the most unforgiving areas of the tax code. What used to be an inconvenience is now a structural tax cost — one that disproportionately affects those who gamble often but profit little.

With the Super Bowl and March Madness coming up, now is the time to understand the rules, tighten recordkeeping, and avoid being surprised next April.

Have questions? Let’s connect.